Coming from China, I've been tracking USD/CNY fairly closely. Directionally, my view aligns broadly with consensus: CNY appreciates. The caveat is one of timing and pace — I'm bullish on the yuan over a 12-month and longer horizon, but I'd expect it to trade roughly flat over the next three months and appreciate only gradually over six.

Thesis

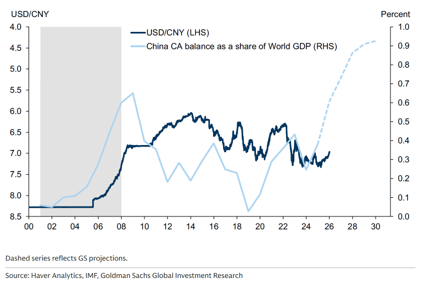

In the near term, there's broad consensus that the yuan is deeply undervalued in nominal terms, and more so in real terms, driven by strong exports against a backdrop of persistent deflation. CPI YoY has run near zero for the past three years and PPI has turned negative. With imports constrained by weak domestic demand and exports up 19.4% in 2025, China's current account surplus has been widening rapidly since 2024.

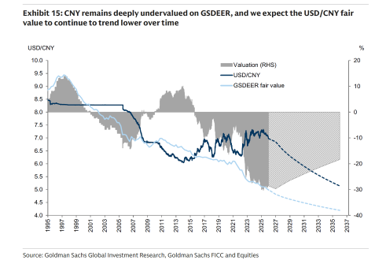

That widening surplus makes the yuan increasingly undervalued on real-exchange-rate measures. As of the start of the year, the IMF estimated the yuan undervalued by 12–21% on REER measures, and Goldman put it at roughly 25% on a trade-weighted basis even at the 6.8 level. So the question isn't whether the yuan is undervalued — it's how fast that gap converges.

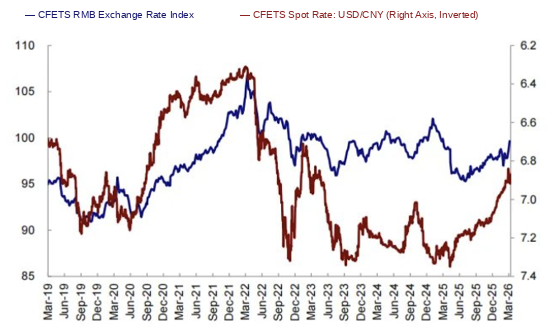

The appreciation began in H2 2025, attributable to a combination of dollar weakness and improved certainty around US–China trade. That momentum has persisted this year even with DXY broadly flat — because the yuan stayed undervalued for the better part of two years, Chinese exporters accumulated large USD reserves to earn the carry, and the initial sharp appreciation triggered a flow unwind. That unwind is itself pulling the spot rate toward its fair value as measured against the CFETS basket.

Six-Month View

I expect this trend to continue driving slow appreciation. The market is still trading below the PBoC fixing level set last December, which I read as a strong signal of continued momentum.

The PBoC's stance leans toward controlled appreciation — it's been guiding the fix lower at a relatively steady pace, and the appreciation hasn't yet threatened exports, since CNY strength against the CFETS basket has been far milder than against the dollar alone. Exports were up 14.7% in April.

That said, I see elevated near-term risk from energy-import exposure and from the fact that the domestic fundamentals haven't shown a clear recovery signal yet.

Medium-to-Long-Term View

Here I'm more constructive, because I expect the structural export driver to keep strengthening. China is well-positioned in technology exports — industrial robots and clean energy in particular. We're already seeing it in the data: lithium battery exports up 40% and robot exports up 33% in Q1 2026. As the energy-transition and automation themes continue to play out, China consolidates a favorable position in the global supply chain.

On the policy side, the RMB internationalization mandate signals a government preference for a structurally stronger currency over time — visible already as energy and commodity transactions begin settling in yuan. Finally, investor sentiment toward Chinese equities is improving, which could pull in portfolio inflows once fundamentals confirm.

Trade Expression and Edge

Over the next twelve months, I see limited edge to monetize directly. The yuan carries negative carry of roughly 3% (the rate differential), so appreciation beyond ~3% — from 6.78 toward 6.57 — is unlikely within six months; the forward already prices that much in. The case improves as the rate differential narrows in the years ahead and appreciation can accelerate.

So I'd rather wait for a clearer strengthening in China's domestic outlook or a fading of geopolitical uncertainty before sizing up. Alternatively, a put spread targeting the 6.7 area captures the directional view while limiting cost against the negative carry.

Catalysts to watch: Chinese fiscal stimulus, a further US trade agreement, and the run of macro data going forward.